Why do houses, gold, and stocks keep getting more expensive? This video explains how money is created, why inflation happens, and why saving cash can lose value over time while investments often grow—widening the gap between the rich and the poor.

The full story

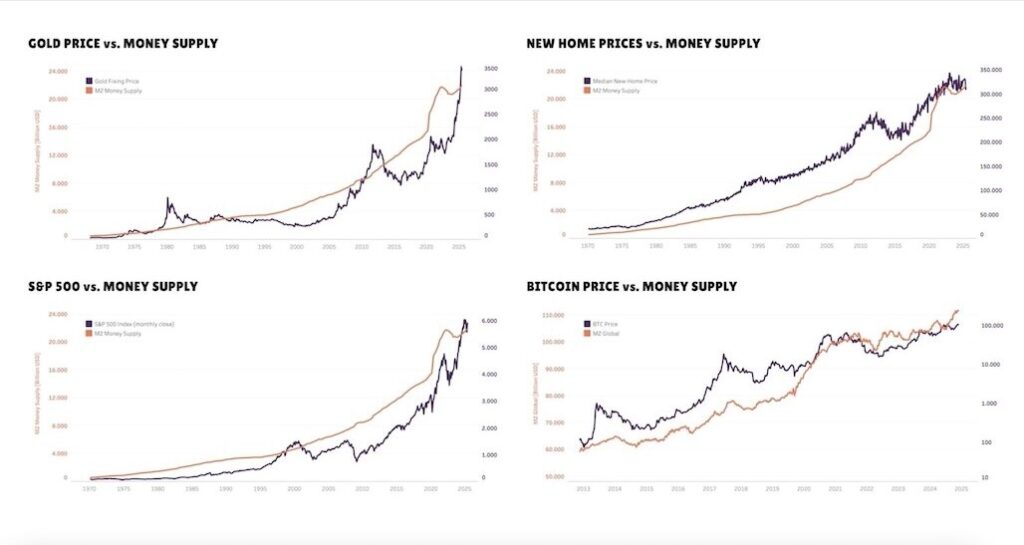

This is the gold price since the 1970s. And that’s total money supplied by the US Federal Reserve. Here we have new home prices and money supply. That’s the S&P 500, which tracks the shares of top American businesses, and money supply. And finally the bitcoin price, here on a log-scale, and – money supply.

If gold, real estate, stocks, and cryptocurrencies all go up with the total cash in circulation, the value of each dollar must go down—which raises some crucial questions.

Why is money losing its value? Who creates it? Why do we keep printing more? And who are the winners and losers of this system?

inflation

The moment you save money, it starts losing value. This happens because bankers and government officials keep printing new money. And so the total US dollar supply increased from around 1.4 trillion in 1975 to about 129 trillion by the end of 2024. And with all the new money, each individual bill lost value.

cash vs assets

To put this in perspective: Suppose your grandparents had—very generously—put 10,000 dollars into a piggy bank for you back in 1975. It’d still be $10,000 today, and would buy you a tiny car. If they had exchanged that same amount for gold, it would be worth $200,000 today — and get you a very fancy sports car. Invested in a fund holding shares in the top 500 US public companies, it would have grown to $2.8 million—you could own lots of cars and a mansion for that!

Bank money

So, how exactly is money created? There are two major forces: bankers and bureaucrats. Bankers create new money whenever they take out a loan. After they approve a credit they literally just type the newly created money into your account—Wohoo. The only requirement: banks must hold about 10% of all the new money they create—And when you repay your loan, the money evaporates again.

central banking

Government officials like to spend more than they actually have. And so they tend to borrow new money from central banks, fund managers, or foreign investors. If such a deal happens with the central bank, it just prints new money. In 2020, the US Federal Reserve created close to $4 trillion this way—which meant that the total dollars in circulation grew by about 26% in a single year.

economic growth

Bureaucrats then typically take this new money, invest it in projects, or give it to particular people and special interest groups. All this new money, so the theory goes, gets people spending and hence creates jobs and economic growth.

But there are not only winners.

the losers

The first losers are those who hoard their cash, unaware that all the new money inflates the price of housing, shares, and other assets.

Second are those who have no access to buy other assets or efficient capital markets and last are those who earn too little to invest in housing, gold, or stocks.

Cost crisis

This last group often faces a double squeeze: They see rent, food and childcare costs rise faster than their paychecks, while wealth-building assets stay out of reach.

share your thought

But what do you think? How could we solve this problem? Should we just stop printing new money? Share your thoughts in the comments below.

Sources

- Money supply – Wikipedia.org

- Quantitative easing – Wikipedia.org

- Global M2 money supply – BGeometrics.com

- Global M2 money supply and Bitcoin – BGeometrics.com

- M2SL: M2 money stock – Federal Reserve Bank of St. Louis

- S&P 500 historical data – Investing.com

- MSPNHSUS: Median sales price of new houses sold in the United States – Federal Reserve Bank of St. Louis

- Shiller PE (CAPE) – In2013dollars.com

Dig deeper!

- Read Inflation: What It Is and How to Control Inflation Rates on Investopedia for a clear overview of inflation and how it is managed.

- Explore money supply and how it is measured in this Macroeconomics course from Khan Academy.

- Watch How Money is Printed on the Beyond Facts channel to see how U.S. dollar bills are produced.

Classroom activity

Objective

Students will understand how increasing money supply affects purchasing power, identify who creates money, and evaluate the winners and losers of inflation.

Materials Needed

- Sprouts video: Why your money is losing value: The economies of money supply

- Whiteboard or chart paper

- Markers

- Scenario cards (savers, investors, low-income earners)

- Student notebooks

Duration: 60 minutes

Steps

1. Introduction and Video Viewing (10 minutes)

- The teacher asks: “If you kept $10,000 for 50 years, would it still have the same value?”

- Collect quick responses, then say: “Let’s watch a short video to understand why money changes in value.”

- Play the Sprouts video.

2. Group Analysis: Tracing Money Flow (15 minutes)

In small groups, students map how money is created:

- Banks (loans)

- Governments/central banks (printing & borrowing)

They discuss: What happens to value when supply increases?

3. Group Presentations and Synthesis (10 minutes)

Groups present their diagrams. The teacher highlights the key concept: more money in circulation → lower purchasing power.

4. Scenario Activity: Winners vs. Losers (10 minutes)

Each group gets a role (e.g., saver, investor, low-income worker).

They analyze: How does inflation affect us? Who benefits? Who struggles?

5. Debate or Discussion (10 minutes)

Class debates: “Should governments keep printing money to stimulate growth, or does it cause more harm?”

6. Personal Application (3 minutes)

Students write: “What would I do differently with money knowing this?”

7. Reflection and Sharing (2 minutes)

Volunteers share. The teacher concludes: “Understanding money supply helps us make smarter financial decisions.”

Collaborators

- Script: Jonas Koblin

- Cartoon artist: Pascal Gaggelli

- Producer: Selina Bador

- Voice artist: Matt

- Coloring: Nalin

- Editing: Peera Lertsukittipongsa

- Sound Design: Miguel Ojeda

- Publishing: Vijyada Songrienchai